I

n

an early draft aimed at exposing the

risks of unfinished trade agreements with China,

Textile World

commented on the likelihood of a new reality of sinking certainty in the outcome of textile

and apparel quota negotiations between the United States and China.

According to sources at the time, both sides agreed to the need for short-term controls, but

true to form, the devil was in the details of defining a practical, substantive growth rate for

Chinese apparel exports to the United States.

Two scenarios appeared likely: First, no agreement would be reached — and no future talks

would be scheduled — and Washington would apply 7.5-percent annual growth caps on exports until

2008, when the specific quota restrictions agreed to by China to gain admission to the World Trade

Organization (WTO) would expire. This solution apparently was unappealing to both sides; but not

sufficiently so to withdraw the last proposal discussed, which offered a menu of growth rates,

dates and bases from which either side could choose.

A settlement has been reached, one relatively consistent with the parameters of the more

generous proposal previously noted incorporating the following features: Ten-percent increases in

apparel shipments and 12.5-percent increases for textiles for 2006. In 2007, rates settle at 12.5

percent in each category, except for fiberglass and thread, which will be allowed to grow at 15

percent annually. Changes in 2008 will include a 15-percent growth against eight products deemed

sensitive by US producers — cotton shirts and pants, bras and underwear. Four other categories —

thread, fiberglass, knit fabric and window blinds — will be allowed to grow 17 percent, with all

other categories limited to 16 percent. The offset has China agreeing to increase the categories

covered up to 34 and, most importantly, agreeing to extend the pact through 2008, a year overlap,

with said caps originally scheduled to evaporate in that year.

With talks settled, industry watchers need to express greater vigilance. A year ago,

TW

published 2002 data about the levels of consumption in Asian mills

(See “

An

Asian Irony,”

TW, November 2004). Information has been updated through 2003, and a 2004

forecast added. This exercise was begun with a search for changes in consumption by India’s growing

and well-managed fabric industries, and with the hypothesis that recent announcements from Indian

government and private sources projected major expansions in man-made fiber and fabric production.

It did not take long for the study to become complicated by United States/China/WTO negotiations,

leading to the analysis presented here.

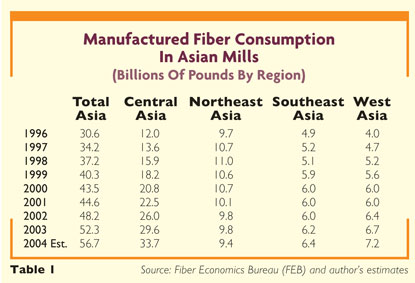

Asian Fiber Consumption

Table 1 details mill consumption of

manufactured fibers — cellulosics plus man-mades — in the larger Asian area from 1996 through a

2004 forecast by the author. By way of identification, the regions are delineated as follows:

• Central Asia — China and Hong Kong;

• Northeast Asia — South Korea, Taiwan and Japan;

• Southeast Asia — Indonesia, Malaysia, the Philippines, Thailand, Myanmar, Singapore and

Vietnam; and

• West Asia — India, Bangladesh, Pakistan and Sri Lanka.

As shown in the table, growth of fiber consumption in all of Asia continues at an almost

double-digit rate, virtually doubling in the 1996-2004 period. As reported last year, the Central

Asian region leads the parade, consuming almost 60 percent of the manufactured fibers consumed in

all of Asia. Further, Central Asian mills account for 11-plus billion pounds, or 41-plus percent,

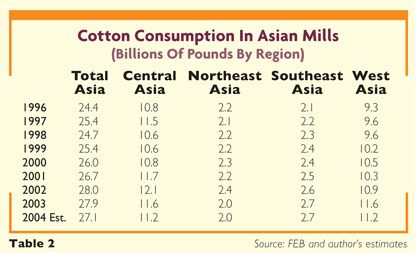

of the total Asian consumption of 27 billion pounds

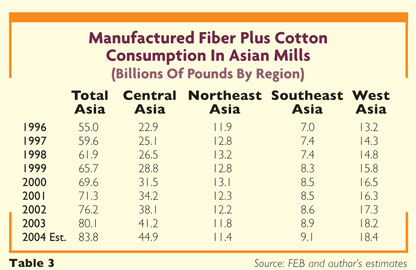

(See Table 2). Together, Central Asian mills consume almost 45 billion pounds of the total

83-plus billion pounds of manufactured fibers plus cotton

(See Table 3).

China and Hong Kong together consume more than 53 percent of all manufactured fibers plus

cotton — simplistically, polyester/rayon or polyester/cotton blends — consumed in Asia. More

significantly, China and Hong Kong together consume 31-plus percent of all manufactured fibers plus

cotton, consumed in the world, assuming an approximate 143-plus billion pounds of consumption of

all fibers in the world. As an aside, Central Asia consumes almost 60 percent of all fibers

produced in the world.

Continuing the geographic tour, as the post-World War II manufacturing economies of

Northeast Asia are replaced by service and banking economic models, manufactured fiber use among

Northeast Asian mills has stagnated, with indications that further contraction will occur in the

future. Japan continues to unravel its fiber, fabric and apparel complex, remaining industry-active

by providing increasing amounts of capital for other Asian regions’ use in growing from undeveloped

to developing nations.

Southeast Asia is made up of several troubled nations, and its performance in the fiber

economy demonstrates this. Weak economies and questionable governments have bred a lack of access

to world capital, and the area has missed opportunities to employ hordes of economically distressed

workers.

Given the speed with which world fiber markets are changing and growing, it is unlikely that

manufacturers in this area can revise policies and practices and join the capital race from

labor-sensitive to capital-sensitive economies. Considering these countries have existed this long

without the fiber industry, it is fair to conclude their agriculture and chemical industries are

aimed at other basic industries, leaving the textile complex battle to other participants.

The Indian Subcontinent

In a move akin to the formation of

the Ministry of International Trade and Industry’s Japan Inc. to guide Japanese industrial growth

after World War II, India has formed several industry/government consortia to provide similar

leadership. India government programs, together with several major product and brand expansions by

Reliance Industries, have led to the Indian presence being felt increasingly in world markets. The

country faces a birth rate that ensures India will house a population larger than China’s within a

decade. With educational access and achievement limited to the few, India appears determined to

structure its economy to offer employment to the entry-level masses in industries such as textiles

and apparel that will generate trade dollars.

Interestingly, cotton consumption in West Asia equals that in Central Asia. Obviously, total

consumption of manufactured fibers plus cotton in Central Asia overwhelms that in West Asia, but an

interesting pattern is developing. Central Asia runs an almost 3 billion-pound net import balance

of manufactured fibers — 10 percent of regional manufactured fiber consumption. West Asia runs a

smaller import balance — only 3-plus percent of manufactured fiber consumption — which raises two

questions. First, are India and its subcontinent neighbors planning to expand man-made fiber

production to soak up more of the area’s supply of cotton and focus the textile complex

increasingly on polyester/cotton apparel exports? Or, are the area participants satisfied with

their current position, secondary to the giant China colossus?

Government programs, reinforced by the actions of Reliance Industries, point to increased

investment in man-made fibers followed by increased exports to the developed world. Ah, the cycle

repeats, although with an unlikely partner.

Where Will It Lead?

What path will apparel imports take

over the next few years? If it’s possible to negotiate equitable import quotas and duties, will the

US textile industry use the breathing room to restructure/remodel/ refinance/redevelop to enhance

its competitive/productivity stance and be ready to compete in a world market?

Based on the situation, it doesn’t look hopeful. Based upon the recent settlement, another

look at China and a more careful appraisal of India, which just may be settling in as a long-time

rival, are needed. After all, if India could last through several centuries of British

rule-fomented confiscatory trade policies, what’s a few years more in a trade war with China over

dominance of international textile trade?

Author’s Note: To simplify graphs and tables, the usage of wool, olefin and miscellaneous

fibers in this analysis has been omitted. For reference, wool consumption totals approximately 1

billion pounds annually across the total Asian region, and olefin does not directly impact the

import/negotiations theme of this article.

November/December 2005