N

onwoven fabrics have seen impressive growth with penetration into a number of filtration

industry end-use market segments. Until nonwovens began to seriously access the market in the

1970s, woven textiles were the material of choice in many industry sectors. Nonwovens offered a

less expensive alternative and often a distinct technical advantage by the basic attributes of the

nonwoven construction. Today, the filtration industry worldwide is growing at 2 to 6 percent per

year above gross domestic product. Even so, the industry’s best years are ahead, with steady and

accelerated growth expected for the foreseeable future.

An assortment of nonwoven baghouse filters used on GE air filter systems

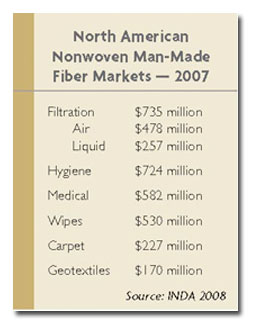

Filtration Market Size

In terms of synthetic nonwoven fabric sales, filtration totaled $735 million in 2007,

according to the Association of the Nonwoven Fabrics Industry (INDA), which reported filtration as

the largest dollar end-use nonwovens market in North America. It is arguably the most profitable

segment. If one were to add in wetlaid cellulose filtration media, total nonwoven fabric filtration

media sales approach $1 billion for North America and $2.1 billion to $2.3 billion worldwide. The

only other filtration media of comparable volume are membranes, with $2 billion to $2.2 billion

worldwide roll good sales in 2007. Together, nonwoven fabric and membrane filtration media dominate

the filtration media market, with more than 90-percent combined market share in terms of roll goods

filtration media volume in comparison to all other material forms. Nonwovens and membranes never

compete with each other in a specific application, as each has its specific advantages, and they

often are combined to complement each other. Typically, nonwoven fabrics add backup support and/or

mechanical strength to comparatively weak membrane media, allowing membranes to function at peak

performance.

Nonwoven fabric filtration media have dominated in applications such as coolant filtration,

baghouse filtration media, vacuum cleaner bags and many heating, ventilating and air conditioning

(HVAC) applications. In these and other applications, nonwovens are highly price-competitive. Yet,

a number of other end-use segments generate impressive profits, especially in liquid applications

when combined with membranes.

Air applications consume approximately 65 to 70 percent of the nonwoven filtration media,

with liquid uses consuming the remaining 30 to 35 percent. Liquid application end-uses tend to

generate higher margins for the nonwovens producer because of the specialized constructions and

performance requirements, particularly in the medical, pharmaceutical and microelectronics

industries. In addition, there are rapidly expanding global needs for pure and potable water.

This pocket air filter from Filtration Group is made of meltblown fabric.

Trends And Drivers

Several factors are driving nonwoven fabric filtration media growth, but two megatrends

dominate. First, manufacturers worldwide are filtering with greater frequency at finer micron

levels to achieve higher product quality. Examples include chemical processing, “produced water,”

mining, food and beverage, including high-purity processes such as pharmaceutical and

semiconductor. Second, environmental thinking worldwide is expanding at an increasing rate in

virtually every segment of our economy. Federal, state and local regulators are enacting laws and

regulations specifically targeted at discharges and waste streams at an accelerating rate. Most

industry followers believe the new administration in Washington will support further initiatives

and regulations, with the filtration industry being a major beneficiary.

Where Nonwoven Fabrics Dominate

To understand nonwovens growth in filtration, one must understand the close relationship with

membrane filtration media. In many liquid applications, microporous and reverse osmosis membranes

are experiencing rapid growth. Most membrane applications are growing by 8 to 10 percent annually.

Those dealing with water and wastewater are growing up to 15 percent per year and more. In

light of requirements for finer levels of filtration in many market segments, a number of industry

experts believe this or even higher levels of growth will be sustainable for many years. The major

beneficiary of membrane growth and market penetration continues to be nonwovens used in combination

with membranes in various configurations. For example, nonwoven wetlaid polyester substrates

support reverse osmosis membranes in spiral wrap modules in a $30 million worldwide nonwovens

market. The modules are found in systems predominantly located in arid regions where seawater is

converted to potable water. Spunbond fabrics are used as pleat supports and separators in virtually

every microporous membrane cartridge sold, accounting for nonwoven sales of approximately $35

million per year.

Nonwoven meltblown and spunbond fabric along with nonwoven glass filtration media are the

principal air filtration media for HVAC – an 825 million- to 850 million-square-meter nonwoven

market in North America. High-efficiency particulate air (HEPA) wetlaid glass nonwoven filtration

media represent an additional 90 million to 100 million square meters. Air filters are found in

end-use markets from general dust filtration to high-efficiency filtration in many different

configurations. These filters are rated by a Minimum Efficiency Reporting Value (MERV) standard,

which rates filters from 1 to 20 in terms of their degree of efficiency. At the high end, MERV 17-

to 20-rated HEPA filters are typically used in situations that require absolute cleanliness for the

manufacture of microchips, liquid crystal display screens, pharmaceutical production and

microsurgery in hospital operating rooms. HEPA filters are primarily constructed from wetlaid glass

nonwoven filtration media, with a smaller portion of the market serviced by polytetrafluoroethylene

(PTFE) membranes laminated to a polyester base substrate for support. MERV 1-16, considered

HVAC-grade filters, are principally constructed of synthetic meltblown, spunbond or glass fabrics.

Overall, 75 percent of synthetic nonwoven media go into commercial markets, such as manufacturing

facilities, offices, theaters, hospitals, cruise ships, casinos and other such markets; with about

25 percent found in residential and general consumer air filters.

Nonwoven fabrics are also used as stand-alone filtration media in pleated cartridges. One

noteworthy example is cartridges, principally spunbond media, in the $30 million pool and spa

market. Other recognized cartridge applications include pleated cellulosic automotive engine

air-intake filters and oil filters on the family car, large semi-rigs and off-road vehicles; as

well as the smallest fuel filters on home lawnmowers, chain saws, power washers and other small

engines. Cellulosic media are relatively inexpensive, and are self-supporting when pleated, a key

factor along with the compatibility of construction materials with fluids and temperatures found

under the hood.

Wetlaid cellulosic and spunbond polyester media that range from 200 to 300 grams per square

meter (g/m

2) are used in pleated dust collection cartridges. In North America, dust collection

media represents a 15 million-square-meter market that is growing at 5 percent per year, according

to INDA. Pleated cellulose- or polyester-based filters offer significantly greater surface area

than needlefelt filter bags for a given space as an alternative filter configuration in baghouse

applications. Typically, dust collection cartridges and baghouse filters are found in manufacturing

environments and facilities that process materials that generate large quantities of fine, airborne

particles or dust. The filters are used to reduce particulate exhaust and prevent spontaneous

explosion when large quantities of fine particles accumulate in factory air.

Although pleated dust collection cartridges are an alternative to needlefelt baghouse

filters, needlefelt filter bags remain the clear industry leader in terms of dollars. Needlefelt

sales approach $120 million in North America and $530 million worldwide, with China being by far

the major driver of growth in recent years. Approximately 10 percent of the baghouse needlefelt

fabrics are laminated with a PTFE membrane providing for finer filtration and/or longer bag life.

Separately, the value of micron rated needlefelt fabrics constructed into liquid filter bags is

approximately $25 million to $30 million in North America and $65 million worldwide. For liquid

applications, nonwoven filter bags are used as final filters and in some cases as prefilters,

prolonging the life of final filters in heavily contaminated streams.

Pictured above is a cutaway of an Entegris Intercept® HSM 20 nm pleated cartridge filter.

Nanofibers In Filtration

Pleated dust collection and engine air-intake filters have a lightweight cover of synthetic

nanofibers over a base substrate of a wetlaid cellulosic or polyester nonwoven in a growing number

of applications. The nanofibers are as fine as 200 to 300 nanometers (nm) in diameter, with the

amount of nanofiber add-on being quite thin in cross-section and typically weighing less than 1 g/m

2 to 2 g/m

2. The nanofibers are laid down over what will become the upstream side of the substrate

using an electrospinning process, and in one case, an ultrafine meltblown process. These nanofibers

create a labyrinth of fibers with pores finer than particles in the incoming air stream.

Particulate deposits and resides on the surface of the fine nanofiber web, allowing the user to

clean the filter by shaking off loose particles from the surface or by using an automated clean-air

back-pulse system. The market is growing rapidly and is becoming an important market sector. All

major suppliers of air filters to the automotive and dust collection market have either internal

manufacturing processes in place or access to nanofiber media from outside suppliers.

By last count, more than 30 companies worldwide have electrospinning manufacturing processes,

but only a few have decent commercial volume. Many have the objective of producing a

heavier-weight, 15- to 90-g/m

2 stand-alone nanofiber web, without the cellulose or polyester base substrate. The

primary goal is to create filtration media to fill the micron rating gap between the finest

meltblown media and microporous membranes. Some manufacturers seek to mimic microporous membrane

micron ratings with higher flow rates. With regard to manufacturing costs, the relatively low

production speed of electrospinning is ideally suited for lightweight covers over substrates in the

dust collection and engine air-intake filters, as these applications require only a few grams of

fiber to cover the base substrate. Thus, heavier-weight electrospun webs have remained a challenge

because of low process throughput and high production cost compared to alternative filtration media

choices. However, there has been some headway by air filtration media producers who seek to replace

glass media in MERV 17-20 HEPA applications. Nanofiber nonwoven filtration media for applications

in the MERV 10-16 range and potentially for liquid applications clearly remains the largest

untapped potential. Should a lower-cost and/or alternative manufacturing process to electrospinning

be developed that can produce 15- to 60-g/m

2 nanofiber filtration media in the $3- to $5-per pound range, enormous opportunities

exist for the first successful producer.

Conclusion

Nonwoven fabric contributions have been an important mainstay for the success of the

filtration industry for many years, and the future is very bright. As the industry grows, new

constructions will be the order of the day, as there are many unmet media end-use needs and growth

opportunities for an innovative nonwovens producer. The filtration market has a large number of

application niches in which customers are willing to pay for performance. Thus, the most profitable

nonwoven fabric producers offer proprietary materials in less than commodity run size for niche or

near-niche applications. Some of today’s mainstays are gradually fading as new nonwoven fabrics

come to market as differentiated constructions for customers seeking solutions to unmet industry

needs.

Editor’s Note: Edward C. Gregor is managing director of Edward C. Gregor & Associates LLC,

a Charlotte-based consultancy that brings new technologies to market and provides merger and

acquisition services in the fiber, technical textile, nonwoven fabric and filtration industries.

March/April 2009