Soaring cotton costs — now more than double year-ago levels — continue to plague the U.S. textile

and apparel industries, with still no definitive answer as to when the price bubble will burst.

Clearly, no immediate relief seems in the offing as today’s big supply-demand imbalance drops

domestic inventories down to 1.9 million bales — some 35 percent under levels prevailing four years

ago. On the other hand, there’s a good chance for some price easing as the year draws to a close,

primarily because sky-high quotes are resulting in significantly higher 2011 plantings. The

National Cotton Council sees a 14-percent increase in domestic acreage this year, probably enough

to yield about a 19.2 million-bale crop — some 900,000 bales more than last year. Equally

important, all signs point to similar upbeat harvest trends in other cotton-producing nations.

Given average growing conditions, this would suggest close to a 7-percent increase in global output

— enough to make for a somewhat improved supply-demand situation.

Speculative Factor

Speculation also has to be blamed for some of today’s cotton woes. But, here too, there are

signs of better days as the year wears on. The Intercontinental Exchange Inc. is finally increasing

its monitoring of big positive positions and demanding evidence that major market participants

prove they have an economic need for the fiber. Hopefully, this will moderate overall demand and

eventually nudge prices lower. Meantime, hoarding has been rampant in China, where that nation’s

farmers are said to be holding onto as much as 9 percent of the world cotton supply in hopes of

getting a higher price for the fiber. But this kind of strategy also has its limitations, because

sooner or later, this cotton will have to come back on the market. Finally, there’s a third kind of

speculation worth noting — namely, an increasing buildup of cotton-containing products. Many

producers and distributors of these items are increasing their inventories as a hedge against

further procurement cost increases. And here, too, the buildup will eventually be reversed. And

when it is, it should also help bring cotton down to more realistic levels.

Downstream Price Pressures

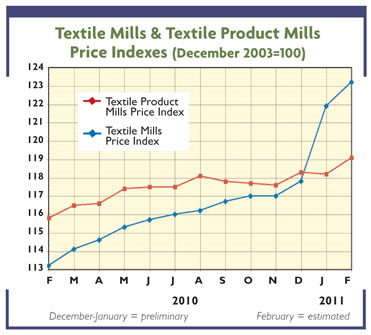

But until the cotton bubble actually bursts, it’s going to be rough going for most textile

and apparel firms — a lot worse than over the past few quarters, when most fabric and garment firms

were able to rely on fiber previously committed for at well under $1 per pound. Hence, a growing

number of new price increases are currently being announced. To be sure, they’re not nearly as

large as those posted for cotton. But that’s not just because cotton accounts for only part of a

textile product’s cost, but also because of increasing substitution of man-made fibers for cotton

and strong buyer resistance. Nevertheless, current and anticipated price boosts still are likely to

be quite substantial, with

Textile World

now projecting anywhere from a 5- to an 8-percent increase in overall textile and apparel

tags for the current year — close to double the advance predicted at the beginning of the year and

well above the nation’s expected 1- to 2-percent overall inflation rate.

Impact On Imports And Profits

There are also likely to be other fallouts from today’s sky-high cotton tabs. U.S. imports of

Chinese textile and apparel products could be affected — primarily because that nation’s producers

may be forced to raise prices even more than their competitors. Such hikes are needed to reflect

two other upward cost pressures — a slowly rising currency and intensifying Chinese internal

inflation. These additional costs could add as much as another 10 percent onto Chinese-made

products. Not surprisingly, Chinese asking prices have jumped to the point at which more and more

U.S. buyers are considering a shift in sourcing — away from Beijing and toward the now-cheaper

offerings of other developing countries. There’s already some evidence of this, with imports from

China beginning to show smaller year-to-year advances. Finally, a few words on cotton and its

impact on bottom lines:

TW

feels 2011 profits and margins may be a bit lower than previously anticipated, reflecting

less-than-full-cost pass-throughs and consumer resistance to higher prices. There will be more

about this next month when updated earnings projections become available.

March/April 2011